Study investing for a week and the first metric you meet is the P/E ratio. It's also the first one you'll misread.

"P/E is low? Cheap stock. Buy it."

That single line is behind a lot of long-suffering portfolios. Let's take P/E from the top and get it right.

What P/E is — in one sentence

The price-to-earnings ratio is:

P/E = share price ÷ earnings per share (EPS)

Put simply, it's "at the company's current earnings, how many years to earn back today's price." A P/E of 10 means ten years to break even, if those earnings hold.

So intuitively, lower P/E reads as cheaper. Half right, half wrong.

The problem lives in the denominator

P/E is built from two parts: price (top) and earnings (bottom). There are two ways it can fall.

- Because the price got cheaper, or

- Because earnings grew — but the market doesn't trust those earnings, so the price didn't follow

The third case is the key. When the market believes "these earnings are about to shrink," it marks the price down in advance, printing a low P/E. Buy it as "cheap" without knowing that, and as earnings actually fall, the price falls with them. This is called a value trap.

Three common reasons P/E is low

Behind a cheap-looking low P/E, there's usually a reason.

① Earnings at a peak. Cyclical stocks (semiconductors, chemicals, shipping) show maximum earnings at the top of a boom — so P/E looks lowest right then. When those earnings roll over, the "low" P/E was an illusion.

② A declining industry. If the market judges "this sector's earnings shrink long-term," it discounts the price now. Cheap against today's earnings isn't cheap if future earnings fade.

③ Hidden risk. Heavy debt, litigation, regulation, or one-off gains that won't repeat — anything saying "current earnings won't last" produces a low P/E.

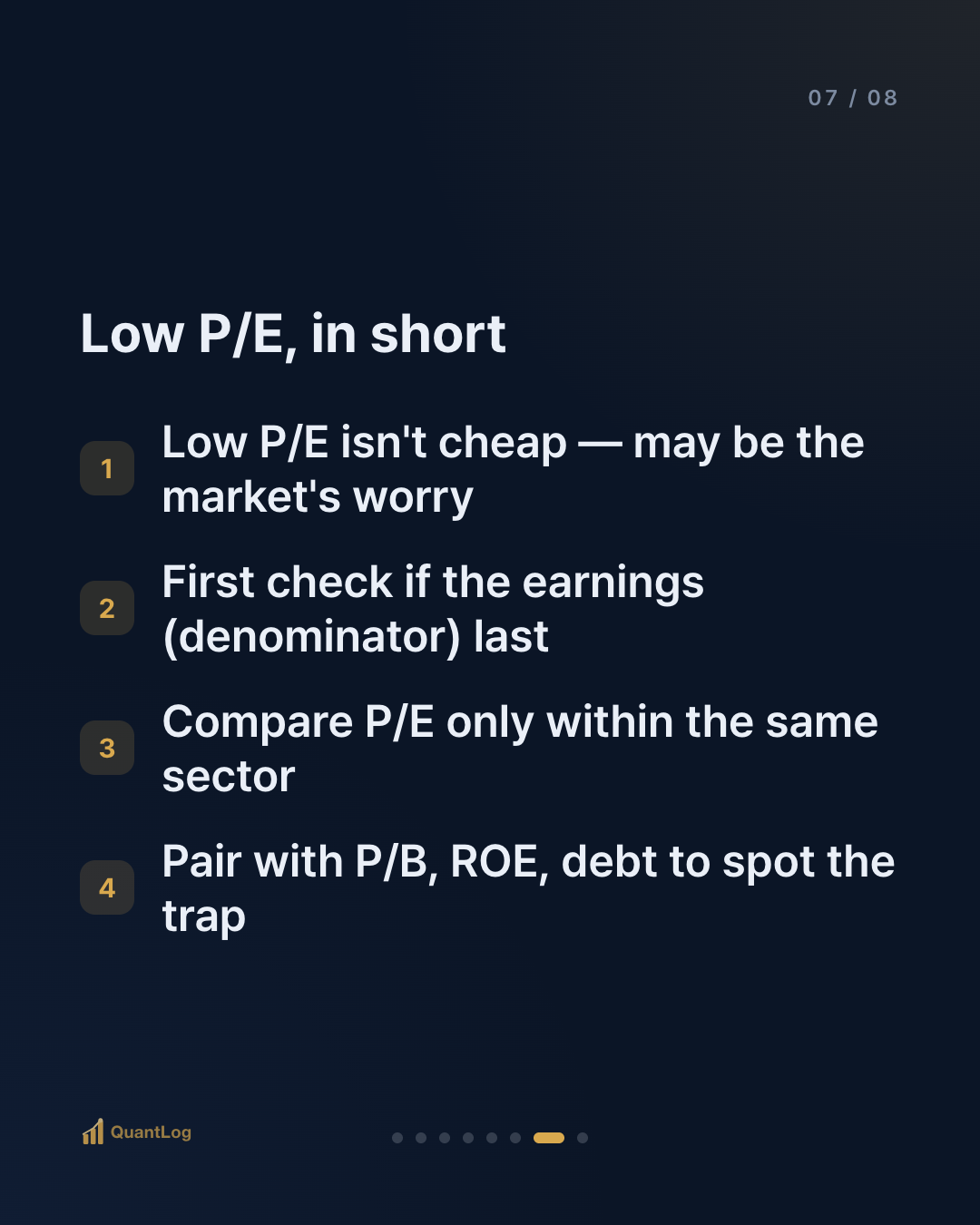

In short — a low P/E isn't "cheap," it may be "the market is worried about something." The real work is deciding whether that worry is overdone or justified.

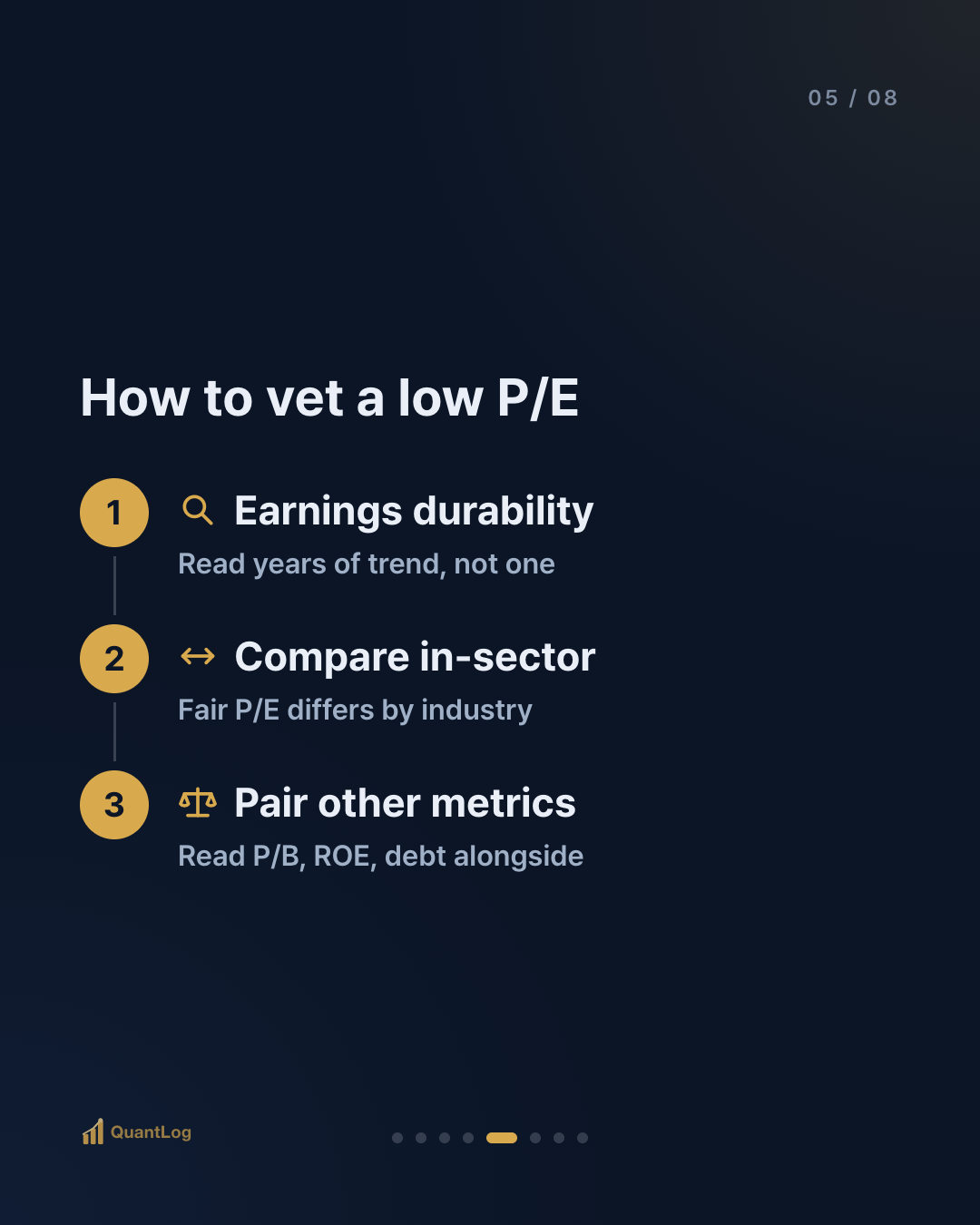

So how should you read a low P/E?

Never P/E alone. Check three things together.

1. Are the earnings sustainable? Look at several years of the trend, not just the last twelve months. If earnings spiked temporarily, that P/E can't be trusted.

2. Did you compare within the sector? A fair P/E differs by industry. Growth sectors run high P/Es; mature ones run low. Comparing P/E across unrelated industries means little.

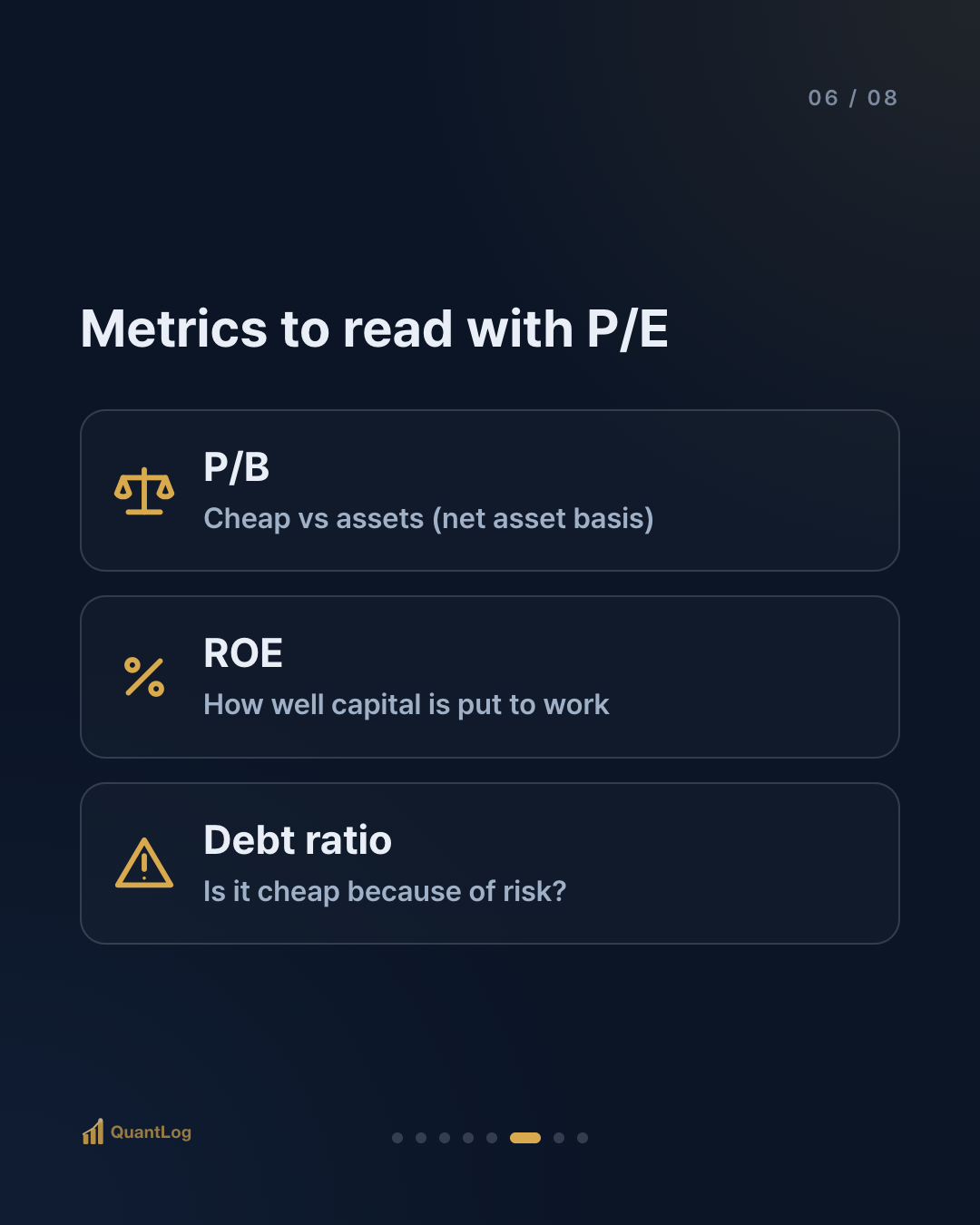

3. Are you reading it with other metrics? P/B (vs. assets), ROE (capital efficiency), and debt ratio reveal *why* it looks cheap. Low P/E + low ROE + high debt is very likely a trap.

In one line

A low P/E is a starting point, not a conclusion. "Cheap" is a verdict you can only reach after checking earnings durability, the sector, and other metrics. Decide a buy on the P/E number alone, and you inherit — late — the risk the market already knew about.

Next up: its partner metric, P/B, dissected the same way.

Disclaimer

This article is for informational purposes only and is not investment advice. It is not a recommendation to buy or sell any security. All investment decisions are your own responsibility.

Comments 0

Be the first to comment.